New York City has been the American city hit hardest by the COVID-19 pandemic. Not all New Yorkers are equally at risk; age has been a serious risk factor, and nearly 75% of New Yorkers who have died from COVID-19 were 65 and over. Race and class also influence infection and mortality rates: Black and Latino city residents have died from COVID-19 at twice the rate of White or Asian New Yorkers, and the ZIP codes in the bottom 25% of average incomes represent 36% of all cases of the disease, while the wealthiest 25% account for under 10%.

Nearly half of the 1.2 million adults 65 and over in NYC are Black or Latino, and more than one-third of older New Yorkers have an annual household income of less than $50,000. This means that older New Yorkers are particularly vulnerable to the virus, and for most of them, the safest solution is to stay home. Yet this mandate brings its own set of challenges for many subpopulations:

The 2020 Census is currently collecting data on every American that will inform federal funding, community planning, and legislative representation for the next ten years. Similarly, we must ensure that we collect and utilize a wide range of data on our clients, including household composition and internet access, to inform a comprehensive outreach and resource allocation strategy during this crisis. Otherwise, inequality among older adults will continue to grow long after the pandemic has subsided.

Do you need help paying your bills? On BenefitsCheckUp.org, you’ll find options in your state to help with utility bill payments, prescription drug costs, and more.

Retirement is supposed to be a time to relax, enjoy simple pleasures, and perhaps check items off your bucket list, like traveling to faraway places. Unfortunately, that worry-free scenario is increasingly rare. Despite decades of working hard and saving, many seniors are finding that unexpected life events have derailed their finances. Medical or dental problems, divorce or widowhood, major home repairs, scams, and stock market losses are just some of the things that can upend your plans.

If financial curveballs in your golden years have left you feeling anxious and insecure, saddled with bills and debt, you are not alone. There are plenty of proactive steps you can take to get yourself back on more solid financial footing. This guide will address some of the common money challenges seniors face, then provide a series of steps you can take to safeguard your finances and respond to a crisis.

10 of the Most Common Financial Challenges for Seniors

Many of today’s seniors were raised not to talk about money, but that can leave you feeling like you’re the only one who’s struggling. You’re not. Even the best-laid financial plans can fall short when life surprises you — and it always seems to do so at the worst possible time. Maybe the bottom dropped out of the housing market right after you put a chunk of your savings into real estate. Or perhaps that part-time job you were using to supplement your Social Security check went away when the coronavirus hit.

Maybe you’re still dealing with the fallout from the 2008 recession, or perhaps an unexpected dental problem cost you a bundle. Unfortunately, there are a lot of events that can sucker punch you financially in retirement. The obvious questions are: What are my options and how do I turn things around? Of course, the answers depend on your situation. Here are some of the most common things seniors like you are facing.

Medical costs

According to Fidelity Investments, a 65-year-old couple retiring in 2019 could expect to spend $280,000 on medical care during retirement. That’s a hefty chunk of change. Cost estimates like these are so worrisome that, in a 2019 AARP/University of Michigan poll, 45% of Americans ages 50-64 said they had little or no confidence that they’d be able to afford health coverage upon retirement. So, if you’re worried, you’ve got plenty of company.

Dental problems

Oral care can get more complicated as you get older, with the cost of root canals, cavities, crowns, or dentures eating into your savings. The CDC reports that 96% of adults 65 and older have had a cavity, and 1 in 5 have untreated tooth decay. That same proportion — 1 in 5 — have lost all their teeth, and slightly more than two-thirds have gum disease. Yet according to the Kaiser Family Foundation, 37 million people, or 65% of those on Medicare, had no dental coverage as of 2019. Half of Medicare recipients hadn’t seen the dentist in the previous year, and 19% spent more than $1,000 out of pocket.

Widowhood

Being widowed is not as big a risk factor for poverty as it once was, but a spouse’s death can still lead to significant financial challenges. Whereas 37% of new widows became poor in the 1970s, that figure fell to between 12% and 15% by the 1990s. Still, a recent Congressional Research Service report on poverty found that the figures haven’t changed much since then: While 4.3% of married women live in poverty, 13.9% of widows do.

Divorce

Poverty rates were even higher for divorced women than for widows in the CRS study, at 15.8%. Divorces can be expensive for both parties, often costing an average of $15,000 per person — and that’s just for the divorce itself. Afterward, you’ll become a single-income household, losing out on financial advantages such as joint tax filing and lower auto insurance rates.

And while a University of Maryland study of divorce rates found the rates dropped between 2008 and 2016, it also found the highest rate of divorce was among those 55 and older, and those who had been married more than 30 years.

Stock market volatility

The Great Recession of 2008 presented huge challenges, and in some ways, the economic fallout from the COVID-19 pandemic has been even worse. From February 2 to March 20, 2020, the Dow Jones Industrials shed 5% of their value, including a single-day decline of 12.9% on March 16. The losses of 2007-2009 were more sustained (at least so far), with the Dow Jones falling 53.7% over roughly a year and a half.

Every downturn is different, with different causes and varying consequences: While the Great Recession was the result of financial imbalances, the pandemic’s financial crash was created by an external factor: the coronavirus itself and the self-quarantine measures meant to contain its spread. In both cases, however, large channels of cash simply vanished, leaving investors with tough choices and hardships.

Major home repairs

Many of us have experienced the frustration of having to call a plumber to deal with a water leak flooding the basement or a roofer to patch a leaking roof. The need for home repairs is seldom expected, and the cost can be difficult to absorb.

Replacing your roof can set you back $5,000 to $10,000. A new septic system will likely cost you at least $3,000 — and perhaps up to three times that much. Replacing an air conditioner, fumigating your home for termites, rewiring your electrical system, and fixing your foundation are other hefty bills you may encounter without warning.

Personal care

As we age, we can begin to require more help, and the costs of at-home care or a nursing facility are significant. The average cost of a home health aide in 2019 was nearly $4,400 a month, and even a semi-private room at a nursing facility can cost more than $7,500 a month. That’s more than what you’d spend to stay at a five-star hotel in Seoul or Brussels, and you’d even have some money left over for a dinner out.

Debt and inflation

If you’re paying off a mortgage, credit card debt or even student loans (did you cosign one for a beloved child or grandchild?), that can eat into your disposable income, too. There’s also the ever-present creep of inflation, which has averaged 2.4% over the past 30 years.

Boomerang kids

Are your kids still living with you, or are they planning to move back? It’s not unusual these days for kids to move back home with their folks (or just never leave in the first place). A survey by TD Ameritrade found that parents expected their kids to move out of the house — and even be able to treat them to dinner — by age 20. But half of young millennials say they plan to move back home after college, and nearly one-third plan to stay for two years or more.

Scams

Senior citizens are often targets for scams via phone calls, email phishing, and other means. Products ranging from bogus medical insurance to counterfeit prescription drugs are commonplace, as are schemes from funeral and cemetery fraud to investment fraud. Identity theft is an ever-present threat. There’s even a scam in which a caller will impersonate a grandchild and say, “Hi, Grandma. Do you know who this is?” in order to establish a fake identity. Life savings can be lost in the blink of an eye.

These are just some of the many challenges you may find yourself facing as a senior citizen. But take heart, because there are steps you can take to minimize your exposure to crisis and prepare yourself for financial challenges. We’ll take a look at these below.

Take Stock to Understand Your Financial Situation

Avoiding a stressful situation won’t make it go away — and neglect could cause it to get worse. Proactively address your money challenges by starting with a thorough and unflinching inventory of your financial standing. Use the checklist below to help you keep track of all the steps you’ve completed. (Each step is explained in greater detail beneath the checklist.)

Tally all your assets and liabilities

List and total up all your sources of debt and the amounts owed for each. And don’t just include the raw figures: Factor in interest amounts and repayment terms, as well. Pay special attention to any credit card debt. This rate bottomed out in 2012 after the Great Recession, but started climbing steadily again after that. As of 2018, the average credit card debt in the 65-74 age bracket was $5,500.

Come clean with your partner

That credit card or personal loan you signed up for without your spouse’s knowledge? It might not be such a good idea. A poll by CreditCards.com reveals that 44% of respondents hide a checking, savings, or credit card account from their significant other. If you’re each accumulating debt without the other knowing, collectively you could end up with twice the amount to pay off, or more. Come clean so you can take a full inventory and know where you really stand.

Analyze your income and spending

Now it’s time to list all your monthly expenses, including both fixed and variable expenses — all of them. It’s easy to remember only your regular monthly bills without considering annual, biannual, quarterly, and other recurring or occasional expenses. So once you’ve listed the easy stuff, ask yourself questions like these:

Do you pay estimated taxes on capital gains, contracting pay, dividends, alimony, or other income sources?

What about annual property taxes? And don’t forget other seasonal housing costs: Do your utility bills go up during winter, when your heater runs more often, or during the summer, when you crank up the AC?

Car insurance payments can be made monthly or in bulk; choose the course that makes the most sense to you, but if you pay every year or six months, don’t forget to leave room for the payment in your bank account.

If you visit the doctor or dentist two or three times a year (or more often), calculate a total for how much these visits typically cost and plan for those expenses, along with any periodic prescription refills you’ll need.

Factor all these fluctuations and additional expenses into your budget. To help you include every regular expenditure, look through your check register, ledger, or any other record you keep of your financial transactions. It’s easy to remember your mortgage and car payments, but did you include your internet and cellphone bill? You may have more regular monthly expenses than you realize. Make a list — or better yet, create a spreadsheet to help you keep track.

Create a budget and emergency fund

Once you know your ballpark amounts, use them to help you devise a budget that covers them as well as your outstanding, incidental expenses — like gasoline, groceries, clothes, pet food and other essentials. And then, stick to it.

With anything left over, set aside an emergency fund. Experts recommend an amount equal to three to six months of regular expenses. Once your budget is solid and your fund is full — and only then — can you use what’s left in the piggy bank to treat yourself to dinner and a movie (or, instead, to start saving up for that gadget or painting you’ve been eyeing or the vacation you’ve been wanting to take).

Monitor your credit score

Since so much depends on your credit rating and its relative health, it’s always important to survey your credit scores and do everything you can to improve them. Even if you have no intention of applying for a loan, close monitoring also can alert you to errors or issues with your credit, including possible incidences of identity theft or fraud attempted by other parties.

Three major credit bureaus track your credit scores: Experian, Equifax, and TransUnion. These are publicly-traded companies — regulated by the Fair Credit Reporting Act and monitored by the Federal Trade Commission. They tally your score based on on-time (and late) bill payments, defaults, and amount of debt you carry.

Because your credit rating can affect everything from your employment and housing prospects to the interest rates you get on credit cards and other bills, it’s worth knowing your score even if you don’t plan to take out a loan. If you stay on top of it, you won’t risk a rude awakening at the last minute if you find yourself in need of cash.

And here’s some good news: You can obtain a free annual credit report by phone, mail, or the internet. Many banks also now update your credit score weekly or monthly on your account page at no extra charge.

Explore all possible avenues of assistance

Next, look into sources of economic aid that are available to eligible seniors. Include tax credits and benefits programs. If you’re a homeowner, you can claim residential energy credits, and if you’re retired from your office job but still working from home, there’s a home office deduction. That’s just the tip of the iceberg, too.

There’s also a host of government assistance programs available for seniors. Benefits.gov offers Benefit Finder, an interactive questionnaire that lets you input your information to help figure out which programs you’re eligible for. Here are a few of the major federal programs for seniors:

Social Security: You can usually apply for Social Security in just 15 minutes via the SSI website. It even offers a retirement planner to help you with the process, detailing when you should apply, what documents you’ll need, and factors that may affect your retirement benefits, among other things.

Medicare and Medicaid:Medicare.gov offers information on:

How to get Medicare and apply online

What Medicare covers and what it costs

Medicare Advantage, a type of health plan offered by a private insurance company that contracts with Medicare to provide Part A and Part B benefits

Medicare and Medicaid Savings programs available to seniors

How Medicare factors in with the Affordable Care Act

Food assistance benefits available to seniors

Coverage for dental, vision, and hearing care

Energy cost assistance, and more.

Avoid taking on more debt

Once you have a handle on your expenses and potential benefits, there’s one more step that’s vitally important: Do not take on more debt! That means for yourself, your kids, or your grandkids. If you’re on a fixed income, think about “fixing” your expenses as much as possible, too (while leaving some room for unexpected bills, of course).

Discuss the possibilities with someone else, preferably someone level-headed whose judgment and motives you trust. Ask questions like: Do I want to include my child or grandchild on my bank or credit card account? Do I want to cosign for a student loan or car loan? Then play out the possible scenarios that could happen with each course of action.

Take into account how responsible your younger partner is, and — just as important — how much debt you could afford to cover if things go wrong. You even might want to start by assuming they will go wrong; that way you’ll know that if they do, you’ll already have made a plan to absorb the extra expense.

Financial Options to Help You Meet Your Money Challenges

You’ve done the difficult groundwork of assessing your financial situation, devising a workable budget, and even researching and applying for senior benefits from the federal government and other sources. Now you can check out other possible avenues to help you grow and/or safeguard your assets.

Get more insurance

Insurance is one way to protect yourself from getting in over your head in the event of a crisis. You’ve got a couple of options when it comes to life insurance:

Term life insurance gives you a certain number of years of coverage, after which you stop paying and the coverage ends.

Whole life insurance can be more complex and work as an investment. It’s designed to be permanent and tends to be more expensive, too.

Be sure to stay on top of your insurance payments: One survey found that seniors were losing $112 billion in life insurance benefits each year by letting their policies lapse or surrendering them. Assess your insurance options with a certified financial advisor who works for you (not for an insurance company) to learn your best options.

Move assets to less risky positions

According to the U.S. Securities and Exchange Commission, allocating assets in a mixture of stocks, bonds, and cash can be a solid strategy. Because these three major categories historically haven’t moved up and down in value at the same time, keeping a mix of investments can guard against losses. Other options, such as precious metals and real estate, also may be worth considering.

The same can be true with diversification: choosing a group of investments rather than placing “all your eggs in one basket.” Professional financial advice can help you make the right choice for you.

Renegotiate major expenses, including debt

It pays to look at the way you’re carrying debt. Are your credit card interest rates too high? You might consider changing vendors. Also, check into your options for consolidating debts at a lower interest rate. You’ve got a few options when it comes to consolidation:

If you’re a homeowner, you can refinance your mortgage — but make sure the money you’re saving are worth the fees you’ll incur.

A personal loan doesn’t carry that risk, but you’ll have to have established good credit to get one.

You could transfer all your credit card debt to a single card if you have enough wiggle room to do so. But you probably won’t find out your credit limit or interest rate until you’re approved.

Moving to a smaller space can have numerous advantages. Time-honored financial advice is that housing expenses should not be more than 30% of your monthly budget. The home that fit comfortably in your budget while you were working may no longer be affordable once your income is reduced in retirement. Downsizing can reduce your monthly rent or mortgage payments, and probably your utility bill, too, since you’d be heating and cooling a smaller space.

There are also psychological benefits to being more selective and mindful about your possessions. Many people who have downsized say their only regret is not doing it sooner. The more you declutter and reduce, the more simplified and satisfied you’re likely to feel. You’ll probably enjoy your surroundings more, and become more productive, as well.

Also, you could clear out the attic and sell those antiques at a yard sale, on eBay, or via another online marketplace to make some extra cash in the bargain.

Sell an annuity

The SEC defines an annuity as “a contract between you and an insurance company that requires the insurer to make payments to you, either immediately or in the future.” People generally buy annuities to help manage their retirement income, and may invest in one of three kinds:

Fixed: Regulated by state insurance commissioners, fixed annuities guarantee a minimum interest rate and are paid out over a fixed number of payments.

Variable: You have flexibility to direct your annuity payments toward various investment options, usually mutual funds, and your payout will vary based on the amount of investment and rate of return. These are regulated by the SEC.

Indexed: Your rate of return is based on the stock market index. State insurance commissioners regulate these.

If you’re hit with a financial crisis, regularly short of money to pay your bills, or in need of greater financial liquidity, you may want to consider accessing money you’ve got tied up in an annuity. It could be worthwhile to talk with your financial advisor about these three options[a] for selling:

Entirety: You’ll sell the whole annuity in exchange for a lump sum, and you won’t receive any further payments.

Partial buyout: You can sell part of your annuity and still receive periodic income without losing your tax benefits. You can sell a few years’ worth of your annuity for a lump sum. After those years lapse, your regular payments will resume.

Lump sum: You could consider selling a portion of the annuity for a lump sum, which would be deducted from future payments.

A few potential downsides to consider: If you sell an annuity too soon after you purchase it, you should realize that the insurance company will charge you a “surrender fee.” Also, if you withdraw money before you are 59½, you may have to pay a 10% tax penalty to the IRS. There may be other tax implications[b], as well.

Go back to work

If you’ve retired, you still have a wealth of experience to draw upon, plus a great résumé. You’ve got institutional knowledge and training that companies have to pay to provide younger workers. There’s nothing that says you can’t put these advantages back to work for you. If you do, you’re not alone. A lot of seniors are re-entering the workforce, and others never left: In a 2017 survey, half of workers 60 and older said they planned to keep working until age 70, and 20% didn’t expect to ever retire.

If you want to find a new gig, there’s full-time, part-time and freelance work available. Job search websites such as Indeed, Glassdoor, Monster, and CareerBuilder match applicants with prospective employers, and networking sites like LinkedIn can help, too.

But there’s nothing to say you need to return to the same line of work. Instead, you could:

Go back to school: Or enter another job-training program and learn a new, marketable skill. Community college and online learning programs abound.

Monetize a hobby: Maybe you spent your career honing a skill you never tried to market, like woodworking, building electronics, or baking. Companies like Craigslist, Yankee Candle, Facebook, and Mrs. Fields all started as hobbies.

Refocus your skill: Retired teachers can become tutors. Retired journalists can become authors or freelance editors. Experts in many fields leave the office and become independent consultants or contractors, working from home.

Some people go back to work to earn extra income, while others just want to stay engaged. Either way, there are plenty of possibilities open to you.

Tap your home equity

There are a few options for using your home equity. If you want to explore them further, consider speaking to a financial advisor. One bit of information worth knowing: Under federal law, you have three days to reconsider a signed credit agreement and cancel without penalty. Here are some possibilities to think about:

Home equity loan: Similar to a mortgage, you agree to repay your home equity loan in installments over a fixed term. But also like a mortgage, your home is your collateral, and you’ll forfeit your home if you stop making those payments. One difference is that you can usually only borrow up to 85% of the equity you’ve accumulated. If you’re interested, consider speaking to different lenders about the various plans they have available.

Home equity line of credit: This is more like a credit card: You can borrow as much money as you need, whenever you need it, up to a certain limit. But again, if you default, you could lose your home.

Reverse mortgage: This is a plan that allows you to convert some of your home equity into cash without having to make monthly payments. It’s an option available to homeowners 62 and older in all 50 states. The money you receive is usually tax-free, and you won’t have to repay it, nor will it impact your Medicare or Social Security benefits. However, when you die or sell your home, your spouse or estate will be on the hook for the debt — and if they don’t have the cash, they might have to sell the house or take out another loan.

There are three types of reverse mortgages:

Single-purpose: Offered by state/local governments and nonprofits

Proprietary: Private loans

Home Equity Conversion Mortgages: Federally insured plans backed by the U.S. Dept. of Housing and Urban Development

Consider having roommates

Roommates? At your age? Well, yes! Think “The Golden Girls.” This arrangement can work especially well if you’re widowed or divorced — but if your kids have moved away and you have an extra room, that can work, too. (Just be sure your significant other is agreeable to the idea, first.)

But remember: If the roommate is paying you rent, or even if they’re working in exchange for a place to stay, they’re not just a roommate but a tenant. Even if you don’t own the property but are renting yourself, a roommate can become your tenant if they’re paying you for the right to stay there — a practice known as subletting.

If you and a roommate come to an agreement, and they promise to pay you a monthly sum but never even give you a dollar, they could still be considered a tenant. You may need to take them to court in order to lawfully evict them, so be sure to speak with a lawyer if this happens.

Make certain you get along well with any potential roommate, and try to make sure the person is trustworthy and dependable before you create a roommate agreement, whether oral or written. Even if they’re friends and you’ve known them for a while, it’s worth thinking twice beforehand. Good relationships have gone sour over bad business arrangements, so ask yourself whether you’d be willing to risk hard feelings if they can’t pay or you don’t get along in close quarters.

Foreclosure or bankruptcy

Extreme steps like foreclosure or bankruptcy should be taken as a last resort, but in some situations they make sense. You have two options under personal bankruptcy law:

Chapter 7, or liquidation bankruptcy, is generally used by people with limited income who cannot pay back all or some of their debt. It discharges a filer’s debts but also requires them to relinquish any assets that exceed state exemptions. (Each state has its own exemptions, so consult a lawyer to find out what they are.)

Chapter 13, or reorganization bankruptcy, allows a defaulting borrower to propose a plan to keep their home by making more payments. The property isn’t sold, and if the plan is successfully completed — usually in 3-5 years — a homeowner can keep the home.

Judicial: This occurs when a lender files a lawsuit, and the borrower has 30 days from receiving notification to make a payment and thus avoid foreclosure. If the payment isn’t made, the property is then sold at auction.

Statutory: Also known as “power of sale,” this type of foreclosure bypasses the court system. If a mortgage includes a “power of sale” clause, the company can send out notices and then carry out a public auction directly if the borrower fails to make a payment within a certain waiting period.

Strict: In a few states, if payments are not made, the lender can file a lawsuit and reclaim the property directly after a waiting period if the amount owed is greater than the value of the property.

Again, if you’re considering any of these possibilities, consult an attorney to determine the best course of action.

Other Smart Ways to Protect Your Finances

Besides the many official avenues you can pursue, there are plenty of other practices you can keep in your back pocket to help you make the most of your money. Consider the steps below to further stretch what you’ve got to spend and keep safe what you’re trying to save.

Keep an eye out for discounts

Many senior discounts are well known, such as the plethora that come with an AARP membership, but there are many others you might not know about. Keep in mind that different deals kick in at different ages: Some start at 65, but you might be eligible for others at age 60, 55, or even 50. Other discounts are available on certain days: Many Goodwill stores offer discounts on particular days of the week, and Ross has a 10% off deal for shoppers 55 and older in its Every Tuesday Club.

Here are just a few areas for which discount opportunities are available:

Transportation: If you’ve ever thought about taking a train to travel around the country, you might also think about a 15% discount off the lowest fare available to seniors 62 and older on most Amtrak routes. Cruise lines, airlines, and bus services also offer a variety of discounts.

Gym memberships: SilverSneakers offers free gym memberships to some group retirees or Medicare enrollees. Other gyms may offer discounts and deals, too. It always pays to ask.

National parks: Seniors 62 and older can get a lifetime pass for admittance to all national parks for $80, the same as a regular annual pass costs. An annual senior pass is just $20.

Books: Amazon offers AARP members a 50% discount on Kindle ebooks, and 10% off on e-readers as well as print and audiobooks. Also, seniors with a valid EBT card or Medicaid can get Amazon Prime at significant savings, at $5.99 a month.

Movies: Several cinema chains offer discounts of varying amounts for seniors 60 and older or 55 and older. Some deals are geared to specific days, while others are available for any evening showing.

Education: Some universities offer discounts to seniors. For example, Ohio residents 60 and older can attend state college classes free when space is available, and the University of Buffalo offers a similar deal. University of Utah students 62 and older can attend classes on a noncredit basis for $25 a semester. Many other deals are available, so check with your local college or university to see if one is available in your area.

Utilities: Some utilities offer discounts for senior citizens. Check with your local utility providers for relief and discount program offerings.

Dining: Hundreds of restaurants and fast-food chains offer a variety of deals. Burger King, Denny’s, Outback, iHop, KFC, Chili’s and Taco Bell are among the businesses that offer discounts. Some are linked to AARP membership.

Groceries: Grocery chains including Kroger, Publix, Food Lion, Fred Meyer, Harris Teeter, Albertsons, and Safeway offer a variety of discounts. They may vary by location or day of the week, so check with your local store for details.

Track your statements, automate your banking

It’s equally important to review your bank and credit card statements, and report any unauthorized purchases. Credit card apps and online banking can make the process easier, allowing you to view balances and statements online anytime.

Consider signing up for these other convenient banking services that can help you track and regulate bills, spending, and other aspects of your economic life:

Many banks send out email alerts when your balance is low, or there’s suspicious activity on credit cards.

Your bank can also send you alerts when a bill is about to come due.

If you enroll in online bill-pay options, you can regulate the schedule for when you pay, even setting up automatic payments.

Direct deposit is another great option that keeps you from delaying or misplacing checks (while saving a few trees in the process).

For those you do receive on paper, many banks offer apps that allow you to deposit checks using your smartphone, with just a click of the camera.

Shield yourself from marketers

To avoid getting calls from telemarketers, you can sign up free of charge to join the National Do Not Call Registry, where you can register your home landline or mobile phone number. This won’t keep all organizations from calling you — political groups, charities, and debt collectors are exempt — but it will help insulate you from scams and unwanted solicitations. After your number is placed on the registry, you can report unwanted sales calls. And even if it isn’t on the list, you can report robocalls that use a recorded message instead of a live person.

Name a backup person

Finally, a prudent overall tip: Be careful who you trust to manage your finances should you become incapacitated. You should have a plan for such a situation, but make sure you put in safeguards and accountability (for example, oversight by a second trusted person).

Loved ones can have a difficult time making important decisions regarding your health and finances if they aren’t prepared ahead of time. So it’s worthwhile to designate beforehand who you want to make those decisions, and then put in place a clear plan that’s easy for them to follow. Be sure to discuss this with your chosen representatives ahead of time to make sure they’re willing and able to carry out your wishes.

Life-changing events such as heart attacks and strokes can happen suddenly, and other debilitating conditions such as Parkinson’s, Alzheimer’s, and dementia can creep up gradually without anyone realizing it. That’s why it’s important to have a plan in place for both your finances and your healthcare — which, in many cases, will overlap.

When you’re creating such a plan, it’s worth asking and answering the following questions:

How do you want your assets to be managed if you’re unable to do so?

Who would you consider a trustworthy agent for your affairs? Who would be a good backup person?

Who should make medical decisions for you if you were in a coma or otherwise unable to make your wishes known?

Would you want to be placed on a life-sustaining medical device?

Would you consider a do-not-resuscitate order? (Known as a “DNR,” this is a medical order issued by a doctor that instructs healthcare providers not to administer CPR if you stop breathing or your heart stops.)

After your passing, do you want to be an organ donor?

Conclusion

There’s a lot to think about when it comes to protecting your finances and making prudent fiscal decisions as a senior citizen. It’s always a good idea to talk to a credit counselor or financial advisor and, in some cases, a lawyer. Government agencies can also provide help, and so can nonprofit advocacy groups. The more information you’re able to provide and the more questions you are prepared to ask, the more helpful it will be in your quest to manage your money and optimize your quality of life.

Home improvements, modifications, and repairs can help older adults maintain their independence and prevent accidents. Work can range from simple changes, like replacing doorknobs with pull handles, to major structural projects such as installing a wheelchair ramp.

Changes can improve the accessibility, adaptability, and/or universal design of a home. Improving accessibility involves things like widening doorways and lowering countertop and light switch heights for someone who uses a wheelchair. Changes that do not require home redesign, such as installing grab bars in bathrooms, are adaptability features. Universal design is usually built in when a home is constructed. It includes features that are sturdy and reliable, easy for all people to use, and flexible enough to be adapted for special needs.

Evaluating Your Needs

Before any changes are made to the home, evaluate your current and future needs room by room. Once you have explored all areas, make a list of potential problems and solutions. Several checklists are available to help you conduct an initial review.

Minor improvements and repairs can cost between $150 and $2,000. Many home remodeling contractors offer reduced rates or sliding-scale fees based on income and ability to pay. Public and private financing options may also be available. Sources of support include the following.

Modification and repair funds provided by the Older Americans Act are distributed by Area Agencies on Aging (AAA). To contact your local AAA, contact the Eldercare Locator at 1-800-677-1116 or https://eldercare.acl.gov.

Rebuilding Together, Inc., a national volunteer organization, is able to assist some low-income seniors through its local affiliates. Visit http://rebuildingtogether.org to learn more.

Local energy and social service departments can assist through the U.S. Department of Energy’s Low-Income Home Energy Assistance Program (LIHEAP) and Weatherization Assistance Program (WAP). You can also search for state-specific tax credits, rebates, and savings at http://energy.gov/savings.

Many cities and towns make grant funds available through their local departments of community development.

Lenders may offer home equity conversion mortgages or reverse mortgages that allow homeowners to utilize home equity to pay for improvements. Learn more by visiting https://www.ncoa.org/economic-security/home-equity/.

Search for additional resources in your state by visiting www.Homemods.org.

Hiring a Contractor

For some repairs and improvements, you may choose to hire a professional contractor without a public assistance program. In that case, keep these important tips in mind.

Make sure the contractor is licensed, bonded, and insured for the specific type of work.

Check with your local Better Business Bureau and Chamber of Commerce to see whether any complaints against the contractor are on file.

Talk with family and friends to get recommendations based on their experiences. Contractors with good reputations can usually be counted on to do a good job again.

Ask for a written agreement that specifies the exact tasks and timeline.

Your agreement should outline the total estimated cost and require only a small down payment. The terms should require balance payment when the job is completed.

Consider asking a trusted friend or family member to help you review the contract and/or monitor work throughout the project.

Americans of all ages are increasingly worried about their finances now that the coronavirus has infected the economy. So far, the media coverage has focused more on the fallout for working families who are struggling to make ends meet, after losing their jobs, and income, as businesses shutter for the foreseeable future. There’s been far less attention to the financial impact on older adults, who are not only at higher risk of serious illness if they get the coronavirus, but also financially vulnerable if the pandemic leads to a sustained drop in their income and retirement savings. Seniors already face significant out-of-pocket costs for their health care and as a share of their income.

It doesn’t take much to imagine how the coronavirus economy could lead to a drop in both income and retirement savings for seniors for an unknown period of time. Older adults 50 and older who lose their jobs in the wake of the pandemic may find it more difficult than younger workers to get jobs and comparable compensation when the economy begins to recover. And, while some of the 12 million adults ages 65 and older choose to work mainly for professional or personal fulfillment, others do so to pay their bills, often to help support their children and grandchildren. More than 4 million adults ages 65 or older who worked at some time during the year were in families with incomes below 400% of poverty, including a disproportionate share of black and Hispanic seniors, according to an unpublished KFF analysis. Older adults who decide to collect Social Security to compensate for lost earnings, but before their full retirement age, will get lower monthly payments than they would have for the rest of their lives.

We recently released new data that paints a fairly dim picture of seniors’ financial resources in 2019 — before the coronavirus pandemic. These 2019 estimates are likely to be a high-water mark for older adults, at least for the foreseeable future, given relatively high unemployment among older workers and volatility in the stock market, which can affect retirement savings.

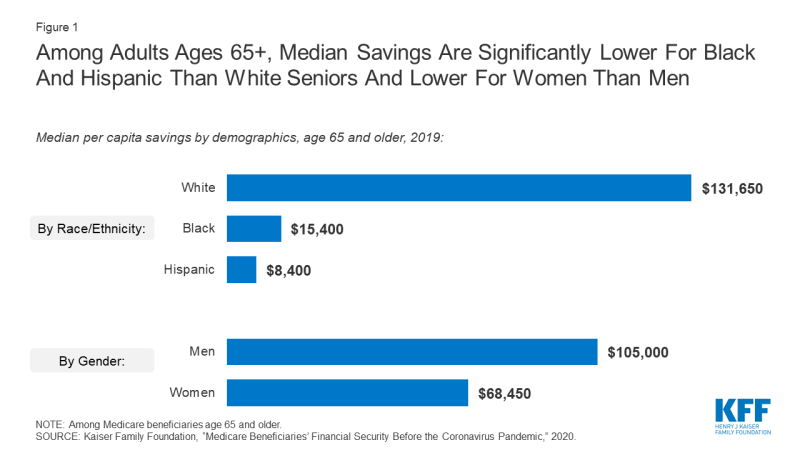

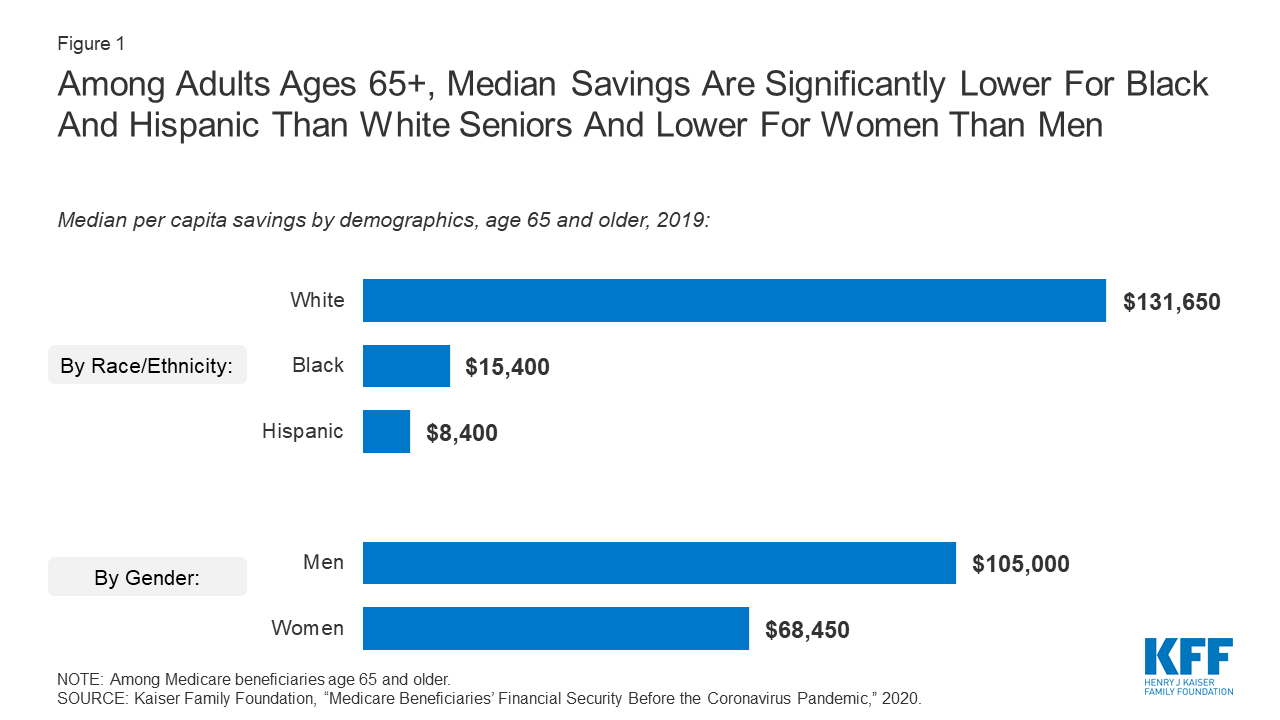

In 2019, as in prior years, the distribution of savings among seniors is highly skewed: the top five percent of seniors had savings of more than $1.4 million per person. However, even before the economy started to falter, half of all seniors had savings of $83,850 or less, a quarter had less than $9,650, and about one in ten (12%) no had no savings at all. Median savings among adults ages 65 and older were substantially lower for black and Hispanic than white seniors, and lower for older women than older men (Figure 1).

Among Adults Ages 65+, Median Savings Are Significantly Lower For Black And Hispanic Than White Seniors And Lower For Women Than Men

For older adults with some or all of their retirement savings invested the stock market, the recent volatility raises uncertainty, more for some than others. The average age 65 and older household with any savings invested about one fifth (18%, on average) of total savings in the stock market in 2016; the share was very low among older households with savings in the bottom savings quintile (<1%, on average) but much higher (36%, on average) among older households in the top savings quintile. The volatility in the stock market raises particular concern for older retirees who have fewer years than younger adults to recover lost retirement savings from a downturn in the economy.

The recently enacted CARES Act aims to mitigate the immediate impact of economic losses on Americans, including older Americans, such as direct payments of up to $1,200 to individuals and more generous unemployment benefits. However, these are short-term solutions to what appears to be a long-term problem. The economic impact of the coronavirus economy on older Americans has important implications for the current response to COVID, and future policy discussions pertaining to Medicare, Medicaid and Social Security.